The Philippines is a top market for global expansion and hiring remote talent. It's located in the fastest-growing region of Asia and has a large English-speaking workforce.

However, navigating payroll tax in the Philippines requires a thorough understanding of the country’s labor laws. If noncompliant, employers may face financial and legal penalties.

This guide outlines everything you should know about payroll and taxes in the Philippines. Learn about mandatory employer contributions, payroll administration options, and how to avoid the risks of noncompliance.

How is payroll calculated in the Philippines?

To calculate payroll in the Philippines, first determine your employee’s gross pay. Then, add the total annual payroll taxes you must pay on your employee’s behalf. In the Philippines, employers must contribute to social security, health insurance, and the Home Development Mutual Fund.

Employers must also add statutory requirements like 13th-month pay and Employees’ Compensation Program (EC) contributions to their total employee cost calculations.

Do you want to calculate how much it costs to hire an employee in the Philippines? Use our employee cost calculator below to get reliable insights into employee costs and payroll contributions in the Philippines:

What are the payroll taxes in the Philippines?

Employers in the Philippines must adhere to a range of local payroll compliance regulations. The four main statutory contributions employers must deduct from employees’ salaries are income tax, social security, health insurance, and the Home Development Mutual Fund.

Income tax

While employers don’t contribute to their employees’ income tax, they must act as the withholding agent by deducting income taxes from their employees’ monthly wages.

The Philippines uses a graduated income tax composed of six income brackets:

- ₱0 to ₱250,000: 0%

- ₱250,001 to ₱400,000: 15%

- ₱400,001 to ₱800,000: 20%

- ₱800,001 to ₱2,000,000: 25%

- ₱2,000,001 to ₱8,000,00: 30%

- Over ₱8,000,000: 35%

Social security

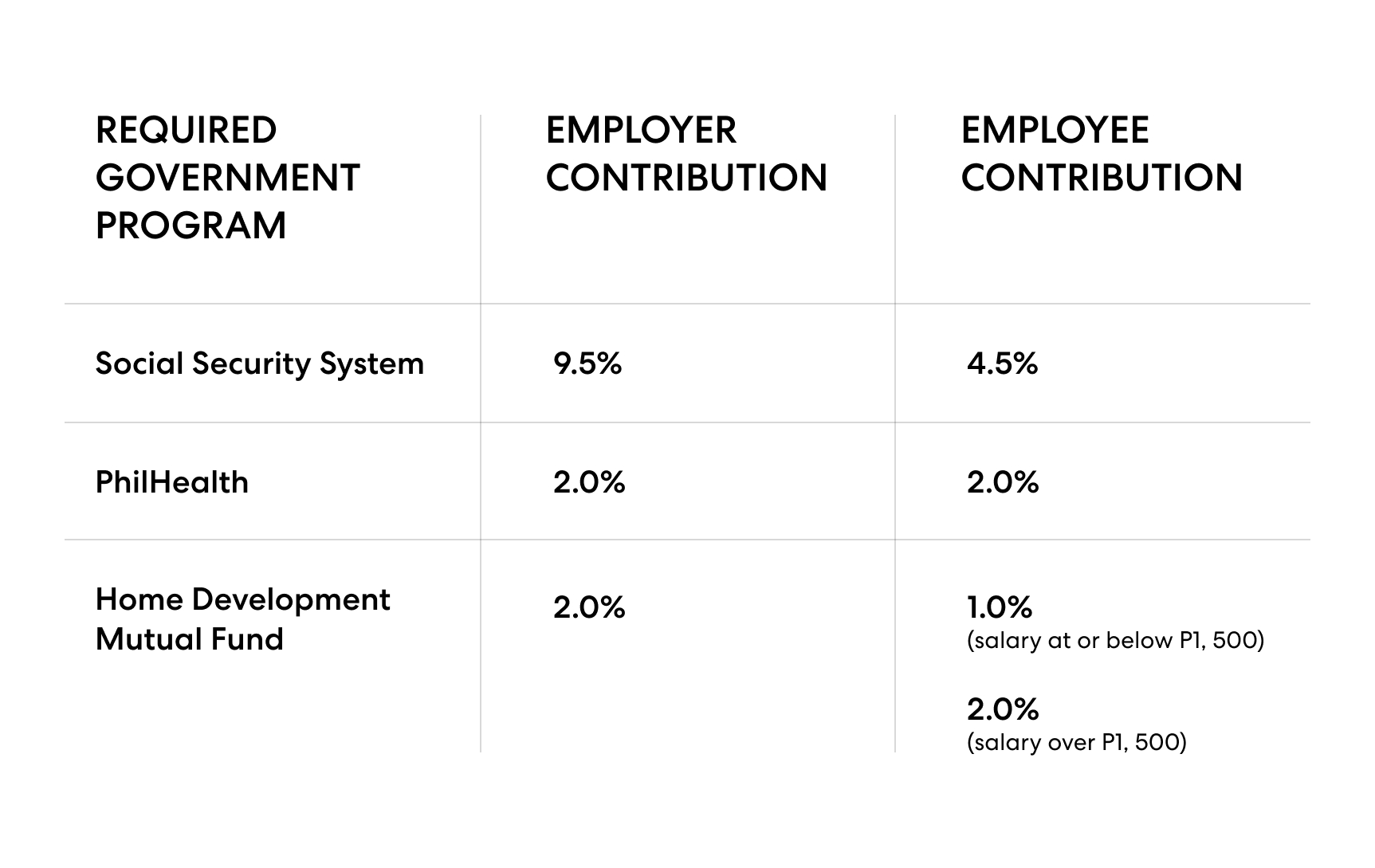

The Philippines’ Social Security System (SSS) is an insurance fund that protects employees from financial burdens related to disability, maternity, sickness, old age, and other contingencies. The monthly contribution rate is 9.5% for employers and 4.5% for employees, with a cap of ₱1,900 for employers and ₱900 for employees.

Philippine Health Insurance Corporation (PhilHealth)

Employers in the Philippines contribute to the state health insurance fund called the Philippine Health Insurance Corporation (PhilHealth). The total contribution rate is 4% of the employee’s base monthly wage, with an income ceiling of ₱80,000. The contribution is shared equally between the employer and employee.

Home Development Mutual Fund

The Home Development Mutual Fund (HDMF), commonly known as the Pag-IBIG Fund, is a government-guaranteed savings fund for employees in the Philippines—though its primary goal is to help employees finance a new home.

The HDMF offers employees low-interest-rate home financing loans with up to 30-year repayment terms and low monthly amortizations. Covered employees also have access to additional benefits under the HDMF, like multipurpose loans and the ability to withdraw their Total Accumulated Value (TAC) after 20 years.

Employers contribute 2% on all employee salaries, while employees contribute 1% on salaries of ₱1,500 or below and 2% on salaries over ₱1,500. Monthly contributions are mandatory for all SSS-covered employees.

Additional payroll contributions in the Philippines

Employers in the Philippines must also contribute to the Employees’ Compensation Program and 13th-month pay.

Employees’ Compensation Program

The Employee Compensation Program (EC) provides employees with financial support for work-related illnesses or injuries. The EC covers any employee in the public or private sector and any employer with a minimum of one employee.

The employer contribution rate for the EC is ₱10 for employees who earn monthly salaries of ₱14,749 or less and ₱30 for salaries over ₱14,749.

13th-month pay

Every Filipino employee who has worked for at least one month within the calendar year is entitled to an annual 13th-month compensation. The 13th-month pay amounts to one-twelfth of the employee’s base yearly income, and employers must deliver it by December 24.

Contractors, commission-based workers, and government employees are not entitled to 13th-month pay—though government employees receive a similar year-end bonus.

Learn more in our guide to 13th-month pay.

Key elements of payroll in the Philippines

Foreign employers doing business in the Philippines must familiarize themselves with the key elements of local payroll policies and procedures:

- Payroll cycle. The payroll cycle in the Philippines is bi-monthly, and employers must make payments twice a month at maximum intervals of 16 days.

- Minimum wage. Minimum wage varies across regions and industries in the Philippines. The minimum wage in the National Capital Region is ₱420 per day in the non-agricultural sector and ₱400 per day in the agricultural sector.

- Overtime. Employees are entitled to 125% of their standard pay for work beyond eight hours in a normal workday.

- Holiday allowance. Employees receive paid time off at 100% of their standard pay on regular holidays but no pay on flexible non-working holidays, like regional events. If they work, employees are entitled to 200% of their standard pay for the first eight hours of work on regular holidays and 130% on flexible non-working days.

- Termination. If an employer terminates a work agreement, they must have a hearing with the employee or issue a 30-day written notice, depending on the cause. Employees who quit must give a one-month written notice unless they resign for a just cause.

- Severance. If an employer terminates an employee for just or authorized causes, the employer must pay either one-half or one month’s wage for each year of the employee’s service, depending on the cause. If an employee voluntarily terminates their employment, they are not entitled to severance pay unless their employment contract or a relevant Collective Bargaining Agreement (CBA) requires it.

Employers must also account for other allowances, like 105 days of paid maternity leave, five days of paid service incentive leave, and the cost of living allowance (COLA).

Learn more about payroll, taxes, and labor laws in the Philippines.

How to set up payroll in the Philippines

Employers who hire employees in the Philippines must familiarize themselves with the country’s tax and labor laws to compliantly administer payroll. Below is a general guide for setting up payroll in the Philippines:

- Register your business as an employer. Register your business with the Bureau of Internal Revenue (BIR) to get an employer identification number (EIN). Your EIN helps local authorities ensure that you accurately calculate and pay necessary taxes and contributions.

- Establish your payroll process and policies. Establish a payroll schedule that details your wage payment and tax remittance frequency, and outline your policies on employee time tracking, payroll tax calculation, and payment methods.

- Determine salaries and ensure compliance. Decide the salary to offer employees based on their role and regional cost of living. Make accurate withholdings and contributions for income tax, SSS, PhilHealth, HDMF, and additional requirements, like 13th-month and holiday pay.

- Collect employee data. Keep a file for each employee’s tax forms, such as their Tax Identification Number (TIN) form, SSS Form R1A, HDMF registration, and PhilHealth Form ER2. Employers should also keep their employees’ primary data on file, such as their name, address, hiring date, work authorization, bank account information, and pay rate.

- Collect timesheets and calculate payroll. Collect and review employee timesheets, calculate statutory tax and payroll withholdings, and make remittances to the relevant government agency.

- Pay employees. Pay your employees according to your established schedule.

- Document and store payroll records. Philippine Labor Code requires employers to document and store employment records for three years. Employers should keep payroll records of dates of employment, pay frequency, total overtime pay, deductions, and net employee salary.

Setting up a payroll process that adheres to Philippine labor legislation is essential for avoiding noncompliance penalties, such as fines, account seizures, and even imprisonment.

Payroll options for employers in the Philippines

Employers have four options for administering payroll in the Philippines: remote payroll, internal payroll, local payroll administration, and fully outsourced payroll.

Remote Payroll

Companies registered abroad can establish an entity in the Philippines to hire local employees and run payroll in the Philippines. With remote payroll, the parent company incorporates the foreign entity’s payroll process into its domestic payroll and administers payroll remotely.

This option streamlines payroll administration, but it requires extra work on behalf of the parent company to familiarize itself with local tax and labor laws. It also exposes the parent company to noncompliance risks.

Internal Payroll

Companies with long-term investments in the Philippines may run payroll in-house for their Filipino employees. This option requires incorporating and registering their business with local authorities. It also requires hiring local staff with the experience to run payroll and accurately fulfill tax requirements.

Internal payroll carries high costs and requires thorough knowledge of local employment and payroll regulations. Employers who choose this route also need a local accounting firm and proper legal counsel to ensure compliance.

Local Payroll Administration

Some foreign companies with registered local businesses outsource payroll administration to a local payroll processing firm in the Philippines. These firms handle all calculations, payments, and filings on the employer’s behalf.

This option offers limited visibility into the payroll process and exposes the employer to security risks. Although a payroll processing firm in the Philippines handles calculations, payments, and filings, the company remains responsible for compliance.

Fully Outsourced Payroll & Employment

The easiest, fastest, and safest way to administer payroll in the Philippines is by fully outsourcing it to a global payroll partner. A global payroll partner is a third-party organization with local expertise that administers payroll for your workforce on your behalf.

By fully outsourcing your payroll in the Philippines to a global payroll partner, you cut costs, save time, and ensure full compliance with evolving local tax legislation.

Even better, foreign employers can quickly hire and pay talent in the Philippines without setting up a legal entity when they outsource payroll to an employer of record (EOR). The EOR serves as the legal employer of your Filipino employees and handles onboarding, payroll, benefits administration, and compliance while you continue to own daily tasks and responsibilities.

A global payroll partner, such as an EOR, administers payroll worldwide, making it an ideal solution for companies with global teams or those eyeing expansion into several global markets.

Learn more: What Is an Employer of Record?

Simplify payroll in the Philippines with Velocity Global

Doing business in the Philippines presents many lucrative opportunities for global companies. Still, the complexities of running payroll in the Philippines deter companies from expanding into this market. Fortunately, the right partner can make a world of difference.

Velocity Global’s Employer of Record (EOR) solution eliminates the risk and complexities of running payroll for your supported employees in the Philippines and beyond. We consolidate payroll into one workforce management platform that facilitates accurate, compliant, and timely payroll and reporting for distributed teams in over 185 countries.

Lean on us to hire, pay, and manage your employees in the Philippines so you can focus on meeting your business goals.

And if entity establishment is in your plans, our Multi-Country Payroll solution allows you to seamlessly and compliantly pay employees in multiple countries where you have entities using one platform.

Contact Velocity Global to learn how to quickly and compliantly hire and pay talent in the Philippines and beyond.